Why Automotive Marketplaces Need a Financing Orchestration Layer

Ten days. That's how long it can take a motivated car buyer in Saudi Arabia to get a financing decision. By then, the car is sold, the buyer is gone, and the marketplace has nothing to show for it but a dead lead. The financing ecosystem isn't broken. The architecture routing it is.

Browsing has never been easier. Financing has never been slower. A buyer finds the right vehicle in minutes, clicks to apply, and immediately hits a wall. One form, one bank, days of silence. Then a rejection. Then another form, another bank, another wait. By the time an approval lands, the moment is dead.

This is not bad luck. It's a design flaw baked into how marketplaces distribute financing today, sequentially, one institution at a time, when the technology to run every application in parallel already exists. Banks, NBFIs, BNPL providers, and leasing companies are all competing for the same buyers. None of them are the problem.

The pipeline connecting them is.

That pipeline has a name: financing orchestration. And closing that gap is the highest-leverage move available to automotive marketplaces in the GCC right now.

How Financing Actually Works Today

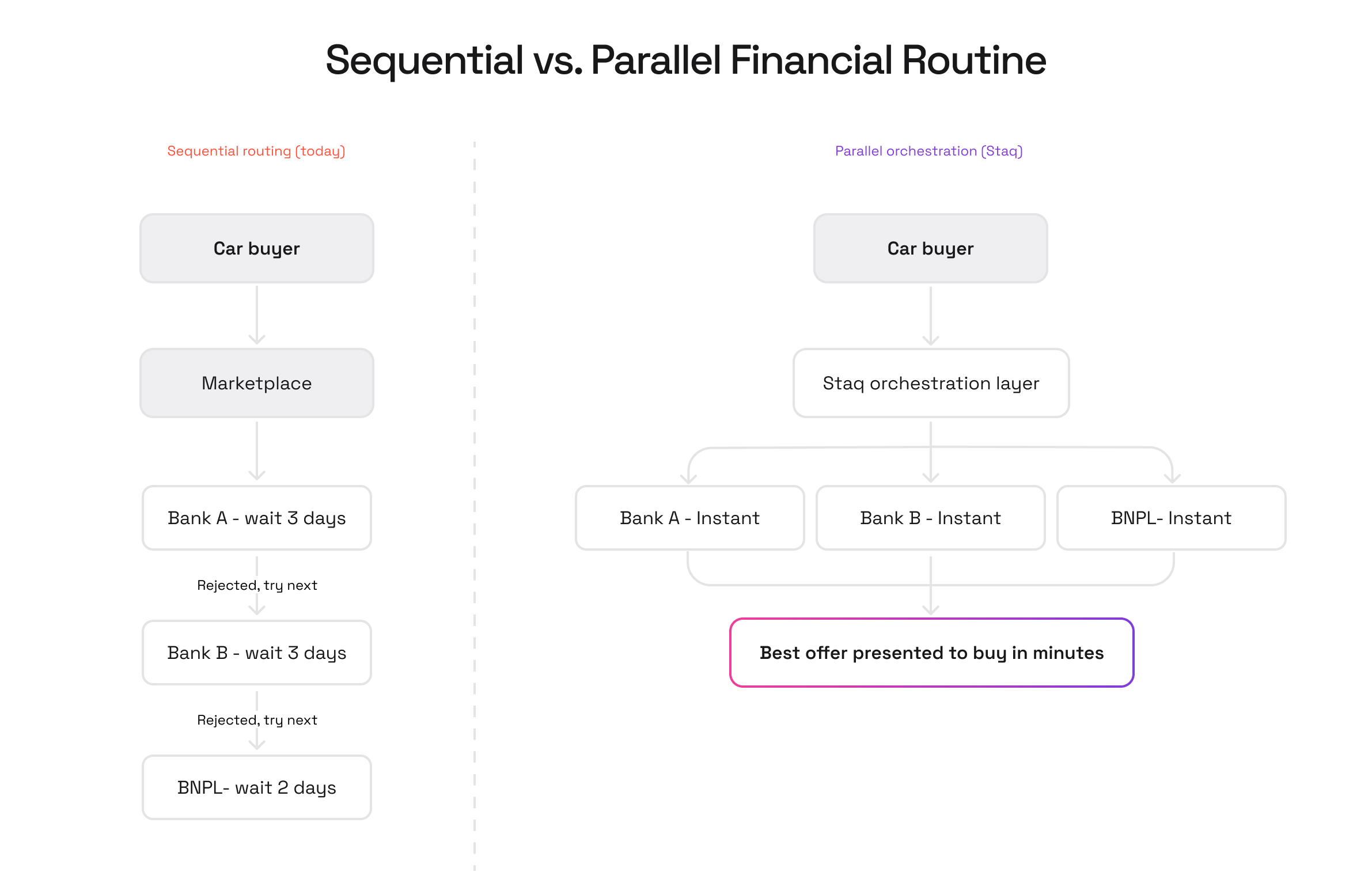

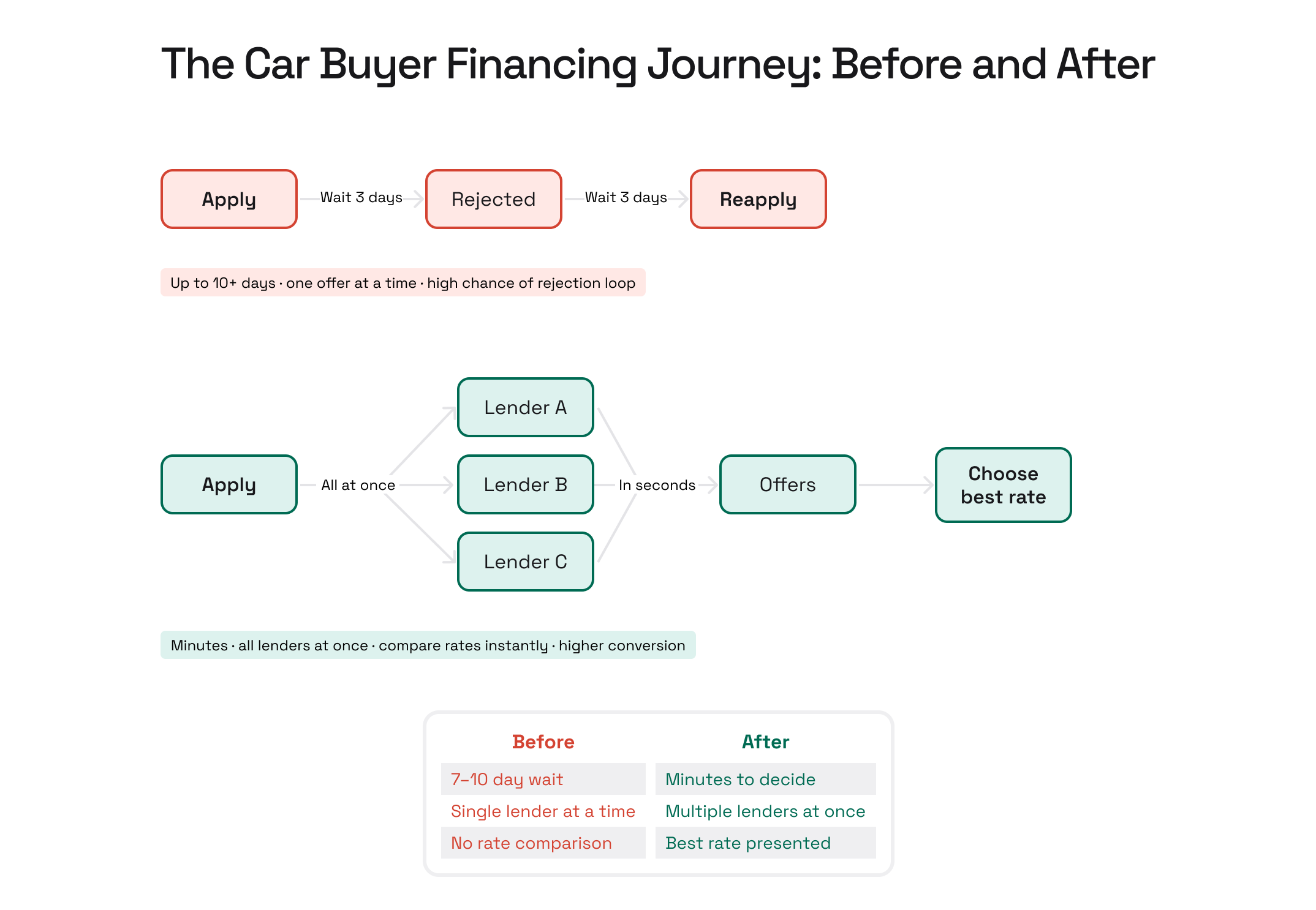

When a buyer on an automotive marketplace decides to finance a vehicle, the current journey typically looks like this. The marketplace collects the buyer information and routes the application to a preferred banking partner. That bank runs its own credit assessment, checks the national credit bureau, applies its internal policy rules, and comes back with a decision in anywhere from two to seven working days.

If the decision is a rejection, the marketplace has two options. It either manually contacts the buyer to redirect them to a different lender, or it loses the lead entirely. Most platforms lose the lead because they don’t control the cycle. The buyer, frustrated and exhausted, abandons the transaction or goes directly to a dealer who has a faster financing arrangement.

The data confirms how damaging this is. Car financing in Saudi Arabia currently takes three to seven working days depending on documentation and bank approval speed, and that is when things go smoothly. When a buyer is rejected and must restart the process, the total elapsed time can exceed ten days[1].

Meanwhile, Cox Automotive research confirms that 97% of dealers report customers who complete steps online and then must repeat them in-store, and 91% of buyers now complete some or all purchase steps digitally before ever setting foot in a showroom. The financing experience is the single biggest point of friction inside an otherwise digital journey[2].

What Orchestration Means in Practice

A financing orchestration layer sits between the marketplace and the financing ecosystem. Instead of routing an application to one institution and waiting for a response before trying the next, an orchestration layer distributes the application to all connected financing partners simultaneously. Banks, non-bank financial institutions, BNPL providers, and leasing companies all receive the application at the same moment, run their decisioning in parallel, and return their offers to the orchestration layer, which then presents the buyer with a ranked comparison of available financing options.

The buyer sees all their options at once. They can compare monthly payments, profit rates, down payment requirements, and tenure lengths side by side. They select the offer that suits them and confirm within the same session. The marketplace retains the transaction. The financing institution gets a higher-quality, pre-consented applicant. The buyer gets a decision in minutes instead of days.

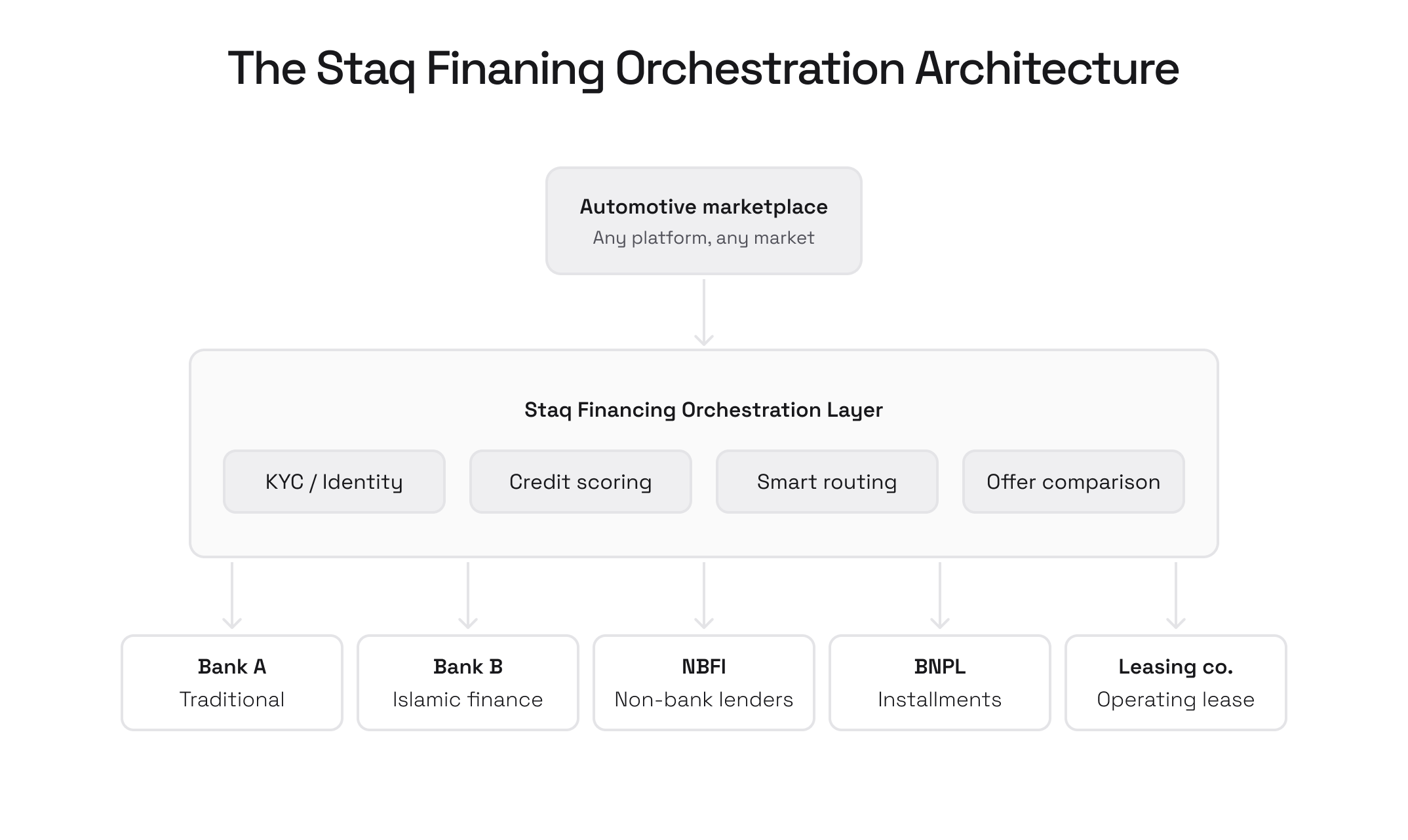

This is not a theoretical capability. The technical infrastructure to run parallel decisioning across multiple lenders already exists. What has been missing is the middleware layer to connect automotive marketplaces to a pre-integrated network of financing institutions, handle the identity verification and credit bureau checks once across all applications, and return structured, comparable offers to the buyer interface.

This is precisely what an orchestration layer built on top of Staq's Bricks platform enables. The Lending as a Service infrastructure handles origination, underwriting logic, and bureau integration. The Digital KYC layer verifies the buyer once and passes that verification to all connected institutions, eliminating the requirement for each bank to repeat the same checks independently. The Payments infrastructure then handles disbursement and settlement once the buyer confirms their chosen offer.

The Numbers Behind the Opportunity

The Saudi automotive financing market is substantial and growing, expanding steadily as Vision 2030 drives urbanization, infrastructure investment, and consumer spending. Meanwhile, the global embedded lending and insurance market is forecast to reach $45 billion by 2028 at a compound annual growth rate of 24.5%, with automotive financing among the highest-volume embedded lending use cases globally[3].

For a marketplace processing five hundred financing applications per month with a current conversion rate of thirty percent due to wait times and single-lender routing, moving to parallel orchestration with a sixty percent conversion rate translates directly into a doubling of financed transactions, without acquiring a single additional visitor. The traffic is already there. The loss is in the financing journey.

There is also a competitive dynamic at work. Dealerships offering captive financing arrangements can approve buyers the same day. Online marketplaces competing with those dealerships cannot afford to offer a seven-day financing journey as their only option. The gap will close, either by marketplaces building orchestration infrastructure or by losing financing-intent buyers to players who have already built it[4].

What The Buyer Experience Looks Like

With a financing orchestration layer in place, the car buyer journey on an automotive marketplace changes fundamentally. A buyer selects a vehicle and clicks to apply for financing. They complete a single digital application, verified once through an integrated KYC flow. The application is distributed simultaneously to all connected financing partners, which may include conventional banks, Islamic finance providers, NBFIs, BNPL companies, and leasing institutions. Within minutes, the buyer receives a comparison screen showing all available offers ranked by monthly payment, profit rate, or whatever variable the marketplace chooses to prioritize.

The buyer selects an offer, confirms their choice, and the transaction moves directly to documentation and disbursement. The marketplace never loses the session. There is no follow-up call, no manual redirect, no waiting period that gives the buyer time to change their mind or find the vehicle elsewhere.

For buyers in Saudi Arabia specifically, an orchestration layer that includes Islamic finance providers alongside conventional banks is particularly significant. Islamic financing structures have specific policy requirements that differ from conventional loan products. An orchestration layer that handles these in parallel, alongside BNPL and leasing options, ensures that buyers who require Sharia-compliant financing are not routed into a separate slow lane.

Beyond Automative: The Same Architecture Applies Everywhere

The orchestration model described here is not limited to automotive. The same infrastructure that allows a car marketplace to distribute financing applications across multiple institutions simultaneously applies equally to any platform where a transaction requires consumer financing at the point of decision.

An education platform can use the same orchestration layer to let parents apply for tuition financing across multiple banks and BNPL providers in a single session, with competing offers returned in real time. A healthcare platform can offer patients a choice of installment plans from multiple financing institutions at the moment they confirm a procedure. A real estate marketplace can distribute mortgage pre-qualification applications across lenders simultaneously rather than directing buyers to a single preferred bank.

In each case, the core infrastructure is identical: a single application layer, a parallel distribution engine, connected financing institutions, and a structured offer comparison returned to the user. The domain changes. The orchestration architecture does not.

This is the broader shift happening in embedded finance right now. The value of Banking as a Service infrastructure is not just in enabling a single financial product. It is in enabling the orchestration layer that makes any number of financial products available to any platform, in any vertical, through a single integration into Staq's Bricks platform. Whether that is cards, lending, or remittances, the modular infrastructure is ready.

What Automotive Marketplaces Should Do Next

For automotive marketplace operators evaluating where to invest in their financing infrastructure, the orchestration layer is the highest-leverage decision available. It does not require replacing existing bank partnerships. It augments them. Existing preferred lenders become part of a broader network rather than being displaced by one.

The technical integration through Staq's Bricks platform is significantly faster than negotiating and building direct integrations with each financing institution independently. The compliance and regulatory framework, including KYC requirements, is handled at the infrastructure level rather than requiring the marketplace to manage it separately per institution.

The competitive window to differentiate on financing experience is still open, but it will not remain open indefinitely. The marketplaces that build this infrastructure now will have a structural advantage in conversion rates, buyer retention, and revenue per transaction that will be difficult for later entrants to close.

If you are building or operating an automotive marketplace and want to explore what a financing orchestration layer would look like for your platform, get in touch with the Staq team.