Exploring the Surge of BNPL: Consumer Trends and Business Opportunities

Buy Now, Pay Later (BNPL) is rapidly transforming the way consumers shop. In the United States, the number of shoppers using this payment option is expected to reach 105 million by 2028, more than double the figure from 2021[1].

But what is BNPL, how does it work, and what is driving its popularity? Let us break down this alternative payment method and tell you how Staq can integrate it into your business.

What is BNPL and How Does it Work?

BNPL is a type of installment loan that allows consumers to make purchases and pay them off later. More and more companies, such as Amazon and eBay, offer BNPL.

Here is how it normally works:

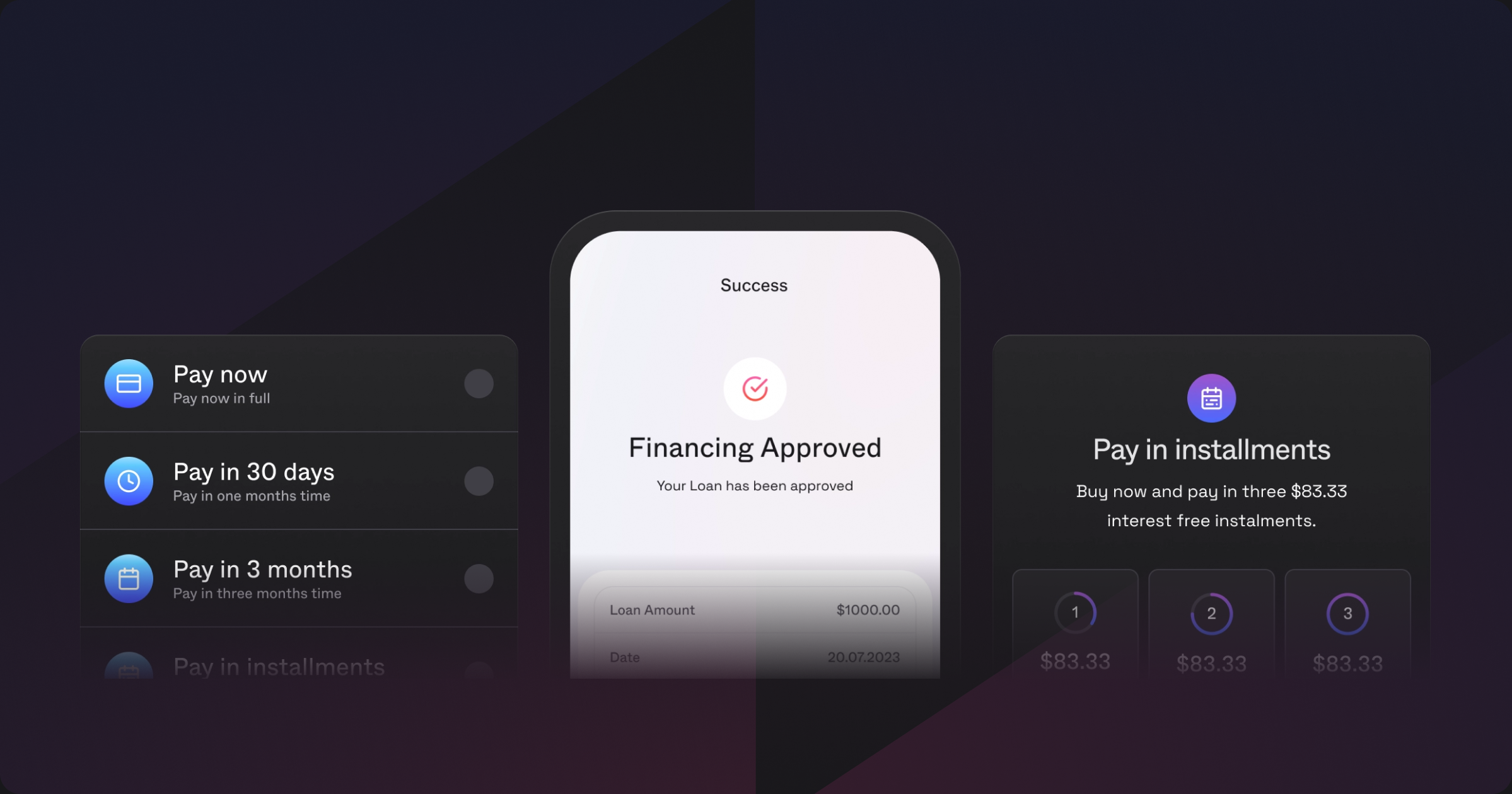

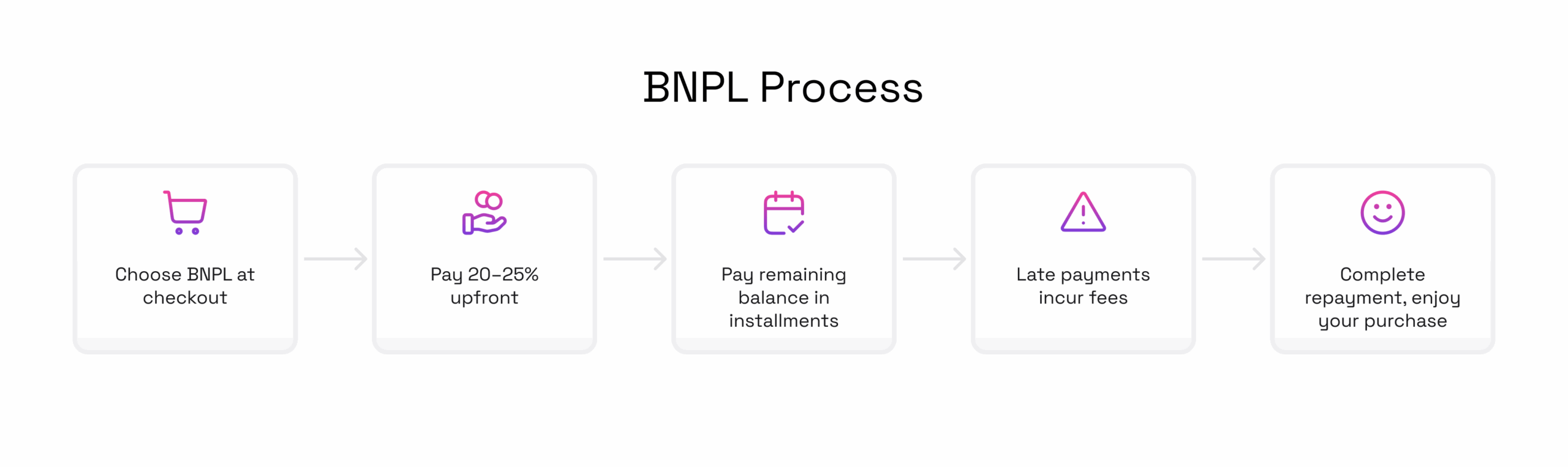

- The customer selects the Buy Now, Pay Later option at checkout, either online or in-store.

- A small initial payment is made, generally ranging from 20 to 25 percent of the total purchase value.

- The remaining balance is repaid over a set period through interest-free installments, usually charged to a debit card or prepaid card.

If the person does not pay off their purchase by the correct date, the lender may charge them penalties and interest.

BNPL is different from other types of financing because it offers short-term and interest-free installments, which might be cheaper and more convenient for consumers. Traditional loans and credit cards charge people interest rates on borrowed funds from the get-go, and they have much longer repayment periods. Consumers usually pay off what they owe over several years.

Why is BNPL so Popular?

Fourteen percent of American consumers used BNPL in 2023[2], up from 12% in 2022. Here are some reasons for increased BNPL adoption and how this financing option addresses pain points for both consumers and businesses.

Benefits for Consumers

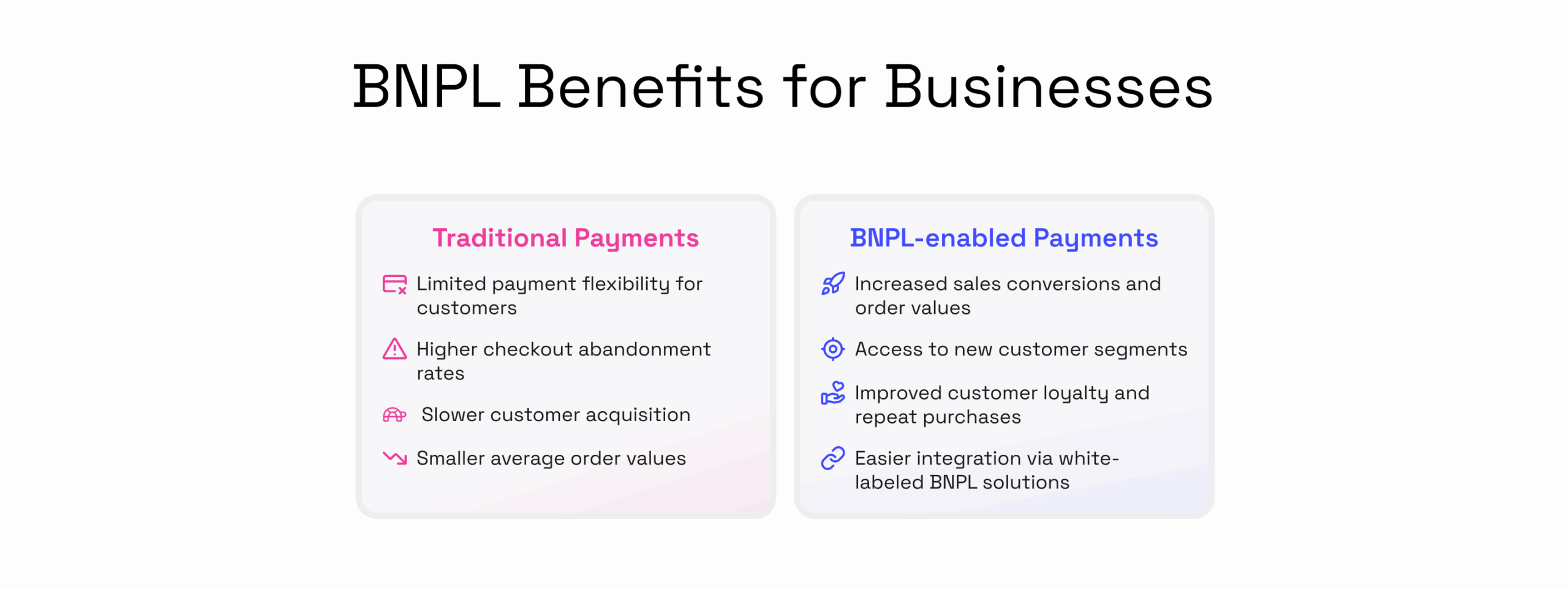

- BNPL empowers consumers to spread the cost of their purchases over time without incurring interest, offering the flexibility that can drive higher conversion rates and average order values.

- A key advantage of BNPL is that it provides credit directly at the point of purchase, creating a seamless and frictionless checkout experience.

The approval process is typically faster and simpler than with traditional credit options[3], making BNPL accessible to a broader audience. - By extending financial access to more consumers, BNPL promotes inclusion and enables individuals to access credit products aligned with their financial needs.

- When repayments are made on time, BNPL generally does not impact consumer credit scores, making it an appealing and low-risk financing option for many shoppers.

Benefits for Businesses

- BNPL enables businesses to benefit from increased sales conversions, acquire new customers, and strengthen customer loyalty.

- Businesses can leverage white-labeled BNPL solutions, simplifying setup and integration while also reducing the cost of implementing BNPL technologies.

- BNPL presents significant business opportunities since by offering BNPL, companies can expand market reach, target new audiences, and unlock additional revenue opportunities.

How BNPL is Changing Consumer Behavior

Prior to BNPL, consumers would either have to pay for a purchase upfront or finance it with a loan or credit card that charges interest. With the introduction of BNPL, people can pay for goods and services over time at no extra cost or minimal fees.

This new approach has significantly influenced consumer behavior. Notably, consumers who use BNPL are more likely to make purchases, with purchase likelihood rising from 17% to 26%[4]. People are also more likely to make bigger purchases, with basket sizes 10% larger on average among BNPL consumers.

So, what is driving these changes? BNPL enables consumers to pay for purchases in smaller, more manageable installments, giving them greater control over their budgets. Compared with traditional loans, which often involve larger payments and longer repayment terms, BNPL can feel simpler and more accessible.

Challenges of BNPL Adoption

While BNPL can drive significant sales growth for businesses, it also raises important considerations around consumer affordability and responsible spending. Research indicates that BNPL users are more likely to have higher-risk credit profiles[5] and lower financial literacy, highlighting the need for careful risk management.

To address these concerns, the industry has implemented regulatory compliance and risk mitigation frameworks that affect companies offering BNPL solutions. For example, in the United States, lenders must adhere to Regulation Z, which enforces the Truth in Lending Act, requiring full disclosure of all fees and charges associated with BNPL products to ensure transparency and protect consumers.

BaaS and BNPL

Banking-as-a-Service (BaaS) is a relatively new business model where licensed banks and fintech innovation companies provide banking products, services, and infrastructure[6] to other businesses. Through BaaS, businesses can expand BNPL services to consumers in different ways, including collecting digital payments, embedding finance options into their companies, and improving credit and lending ecosystems.

A BaaS platform enables the seamless integration of BNPL solutions into a company’s website, allowing businesses to provide this flexible retail payment option without the need to invest in new digital infrastructure.

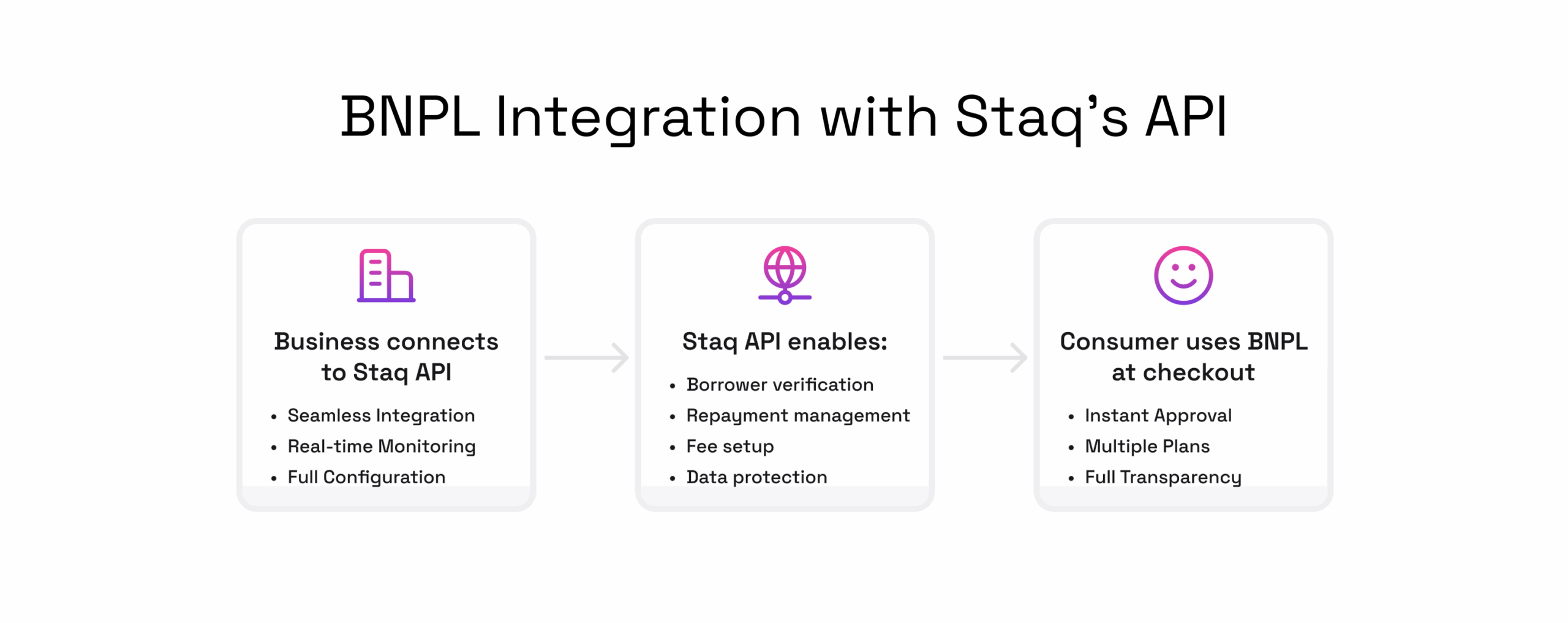

How Staq Can Help You Integrate BNPL Into Your Business

Buy Now, Pay Later, which is increasing in popularity, offers various benefits for consumers and businesses. By incorporating this financing option, businesses may be able to acquire new customers, reach new markets, and ultimately boost sales.

Nevertheless, setting up BNPL can be tricky, as businesses will need to comply with industry rules and invest in infrastructure that ensures everything goes smoothly. This is where Staq comes in. Our innovative, dependable API lets you build and launch BNPL products with ease. We simplify the BNPL process with a reliable, fully compliant API that enables you to launch BNPL products quickly. You can manage borrower verification, loan repayments, non-payment fees, and data protection, all while staying aligned with local regulations.

Ready to scale? See how Staq can help your business thrive. Book a demo today.