Embedded Finance Beyond Payments: What Comes After the Wallet

Ask most people what embedded finance means today, and they will describe a wallet. A digital balance sitting inside an app. A button that moves money. A checkout experience that feels a little smoother than going to a bank. That mental model is not wrong, but it is incomplete.

The wallet is where embedded finance starts. It is not where it ends.

Businesses that have treated payments as the finish line are already falling behind the ones that understood payments as a foundation. In 2026, the gap between those two groups is widening rapidly. According to Bain and Company, embedded finance transaction value is forecast to exceed $7 trillion globally by 2026, more than doubling from $2.6 trillion in 2021[1]. Payments and lending are the largest segments today, but the fastest growth is now happening in insurance, card issuance, working capital, and cross-border services. The wallet unlocked the door. The businesses winning right now are the ones that walked through it.

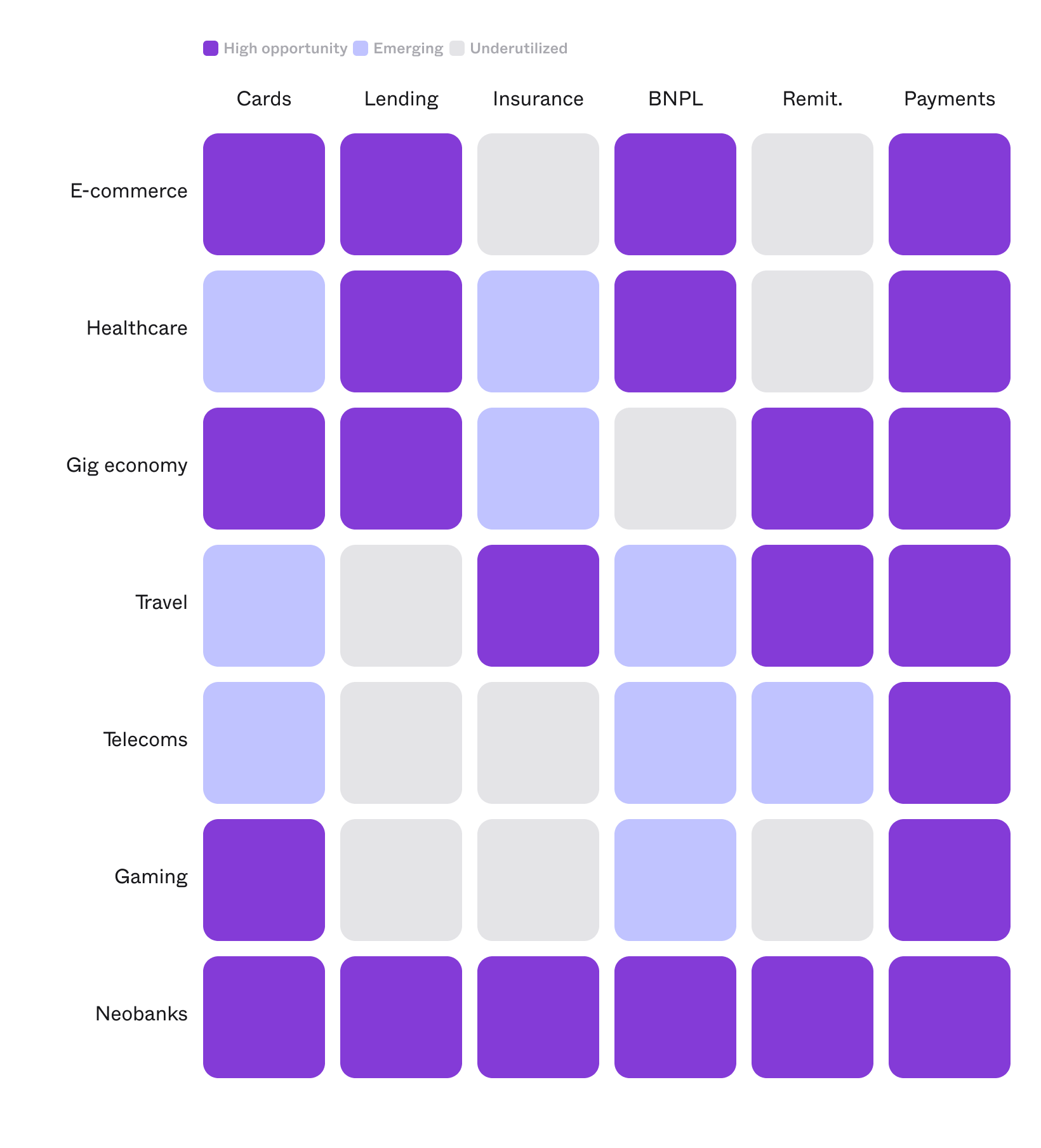

This post is for the CTOs, product managers, and operations leads who are ready to ask a harder question: what financial products should we be offering our customers that we are not offering yet? Below is a matrix that offers a quick view of where embedded finance is gaining the most traction across different industries. By mapping key financial products against sectors, it highlights where opportunities are strongest and where there is still room to grow, helping you frame where your business can focus its efforts next.

The Wallet Was a Starting Point, Not a Strategy

Embedded payments solved one problem: friction at the point of transaction. A customer should not have to leave your platform to pay, transfer, or receive money. That problem is largely solved for the businesses that have already integrated a payments layer.

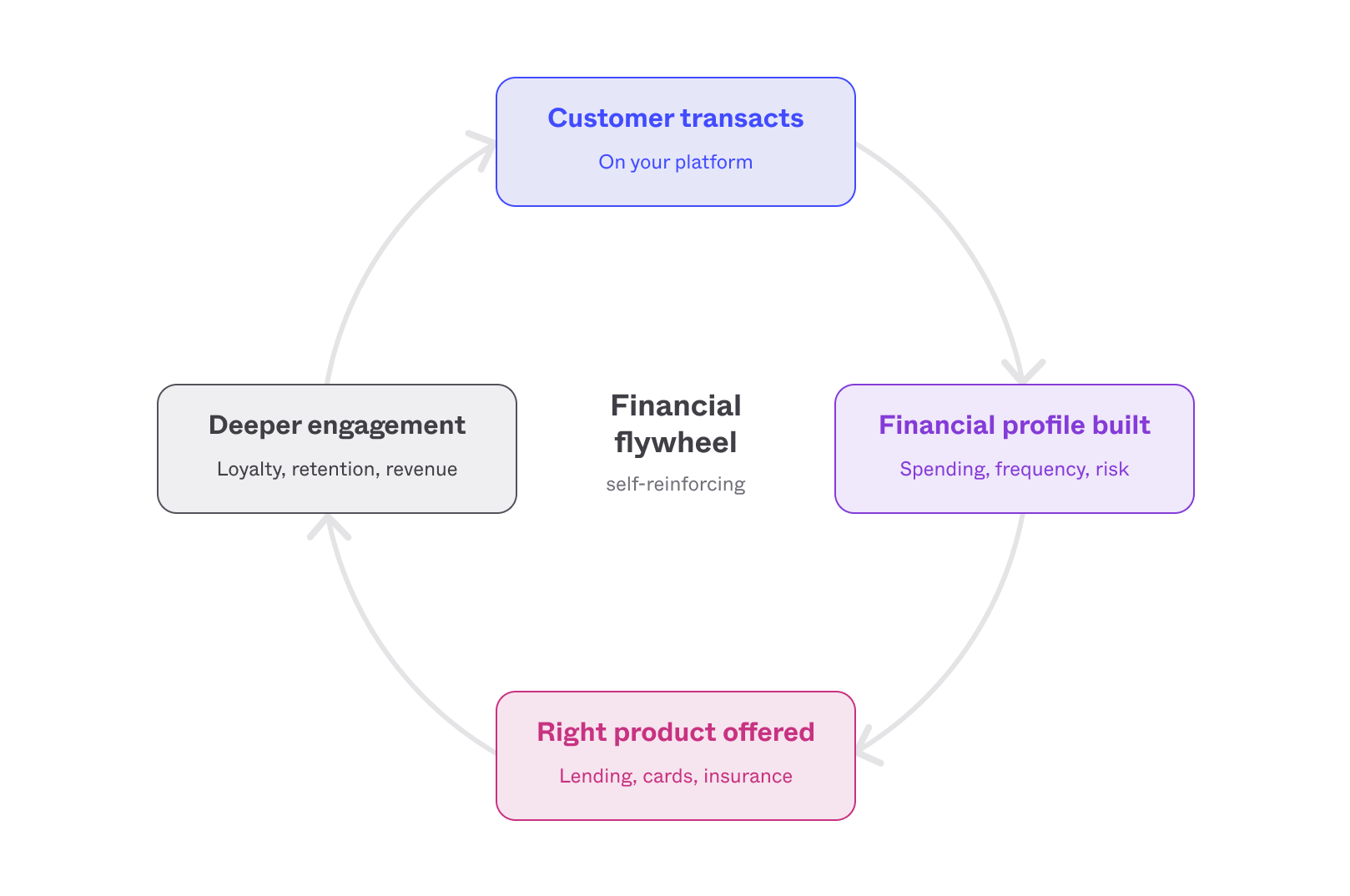

But the financial relationship between a platform and its customers does not begin and end at the payment.

When a user transacts on your platform, you are building something more valuable than a payment history. You are building a financial profile: what they buy, how often, how much, when they need credit, and what risks they carry. Most platforms collect this data and do nothing with it financially. The businesses leading the next wave of embedded finance are using that data to offer the right financial product at the right moment, whether that is a loan, an insurance policy, a card, or an installment plan.

The shift is from embedded payments to embedded finance. From a feature to a full product strategy.

Embedded Lending: Credit Where It Actually Belongs

Embedded lending is arguably the most transformative financial product a platform can offer, because it solves a problem at the exact moment it exists. A merchant on a marketplace platform receives a working capital offer based on six months of sales history. A patient at a private clinic is offered an installment plan at the moment they need a procedure. A gig economy driver unlocks a micro-advance against their weekly earnings before the weekend.

None of these experiences require the customer to visit a bank, fill in a paper application, or wait three days for a credit decision. The platform already has the data. The infrastructure just needs to be in place to act on it.

The global embedded lending and insurance market reached approximately $12 billion in 2023 and is forecast to reach $45 billion by 2028 at a compound annual growth rate of 24.5%[2]. The growth is not happening at banks. It is happening inside the platforms where customers already spend their time.For businesses ready to add lending to their platform, Staq's Lending as a Service solution provides the full infrastructure to originate, underwrite, and fund personal loans, business loans, and lines of credit directly within a platform, without building or maintaining the financial plumbing internally.

Cards: Putting Your Brand in Your Customer's Physical and Digital Life

A branded card is one of the most visible and attractive financial products a platform can issue. Every time a customer pays with your card, regardless of where they are or what they are buying, they are reinforcing their relationship with your platform. You earn interchange revenue on every transaction. You gain richer spending data. And your brand travels with your customer into every purchase, far beyond the moments they are actively inside your product.

The use cases are broader than most businesses realize. A healthcare platform issuing prepaid wellness cards for employee benefit programs. A gaming platform enabling instant payouts to players through virtual cards tied to their in-game earnings. A gig economy company issuing workers a physical card linked directly to their earnings wallet, eliminating bank transfer delays and the friction of cashing out. A neobank offering a co-branded card as part of a loyalty program for a retail partner.

Staq's Cards product allows businesses to issue both virtual and physical prepaid cards with instant funding, dynamic spending controls, and real-time transaction management, all through a single API integration.

BNPL and Remittances: Owning the Full Financial Journey

Buy Now Pay Later has moved from a novelty to a baseline expectation across retail and e-commerce. The BNPL market is forecast to reach $576 billion in global transaction value by the end of 2026[3]. The businesses that are winning in this space are not the ones redirecting customers to BNPL providers at checkout. They are the ones that own the BNPL experience entirely, under their own brand, with their own customer relationship intact.

Remittances tell a parallel story for markets like MENA, where cross-border money movement is a daily reality for millions of workers and families. The platform that offers a competitive, fast, low-cost remittance service earns a financial relationship that extends far beyond shopping or services. It becomes part of how people manage their money, month after month.

Staq supports both Buy Now Pay Later and cross-border remittances as native capabilities within the Bricks platform, not third-party redirects, but fully integrated financial products delivered under your brand.

The Infrastructure That Makes All of This Possible

The reason most platforms stop at payments is not ambition. It is architecture. Adding lending means a new provider. Adding cards means another compliance framework, another API contract, another team managing another vendor relationship. Each new financial product becomes its own project, and most teams do not have the capacity to run four projects simultaneously.

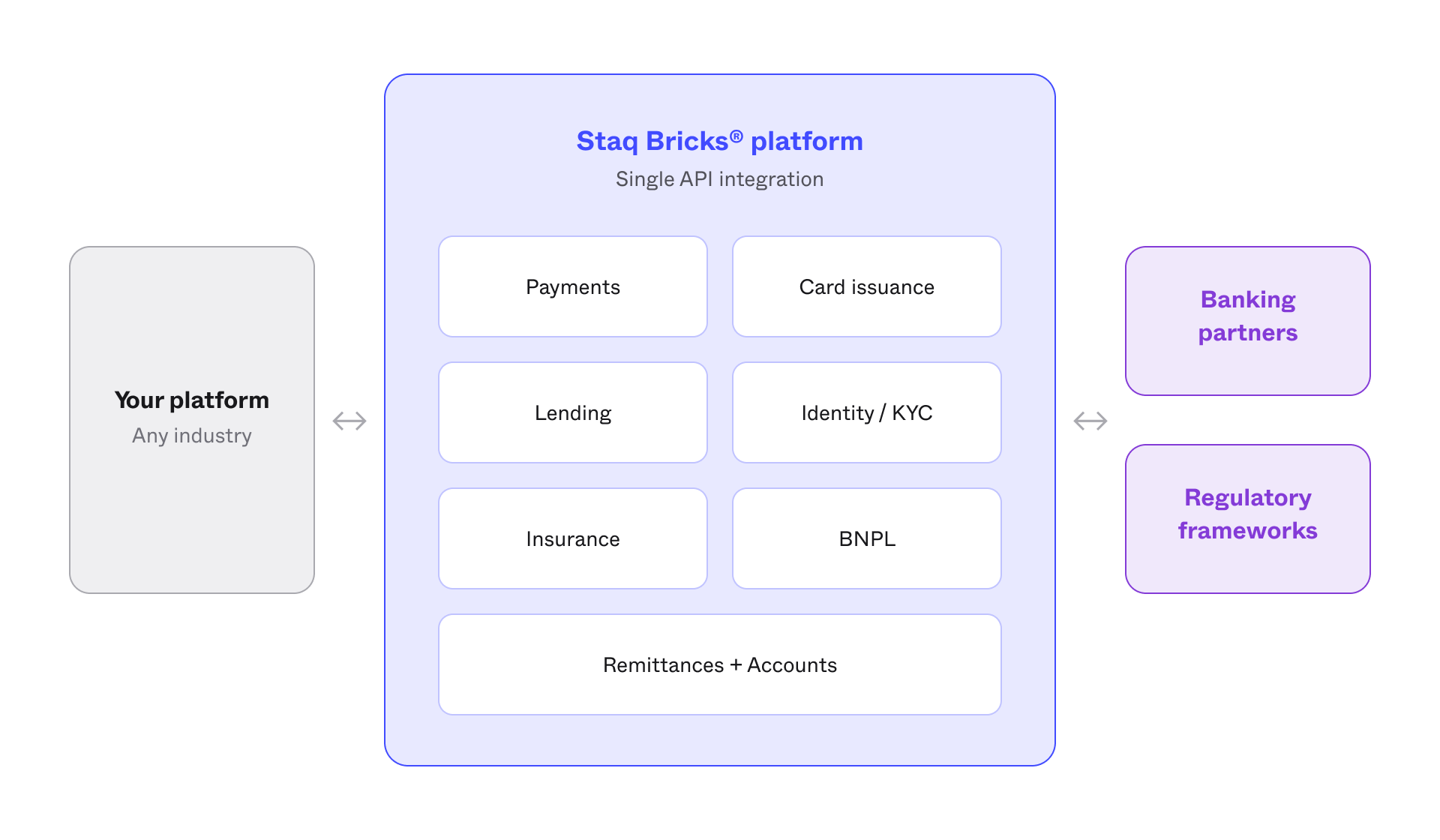

The smarter path is a modular infrastructure where every financial product a platform wants to launch is a configuration decision, not a new build. Account management, payments, card issuance, identity verification, and credit origination all live on the same layer, accessed through a single API, with compliance frameworks and local bank partnerships already built in.

This is what Staq's Bricks platform was designed to deliver. The modular architecture brings together payments, card issuance, digital identity verification, and lending under a single integration layer. Whether a business operates in e-commerce, healthcare, gaming, travel, or telecommunications, the infrastructure is ready to support the full financial product roadmap, not just step one.

The Question Worth Asking Today

The businesses that will define the next wave of embedded finance are not fintech startups building financial products from scratch. They are the retailers, logistics platforms, healthcare providers, telecoms, and marketplaces that already have the customer relationship, the transaction data, and the brand trust.

The financial products are the next natural layer on top of what they have already built. Your customers are already transacting on your platform. They already trust your brand. The infrastructure to turn that trust into a full financial services offering has never been more accessible or more straightforward to integrate.

The wallet was the starting point. The full financial platform is where the real value is.

If you are ready to explore what your next embedded finance product could look like, get in touch with the Staq team.